All Categories

Featured

Table of Contents

The disadvantages of infinite banking are usually ignored or otherwise pointed out whatsoever (much of the information offered about this principle is from insurance coverage representatives, which might be a little prejudiced). Just the cash worth is growing at the returns rate. You additionally need to spend for the expense of insurance, charges, and expenses.

Companies that use non-direct recognition finances may have a reduced reward price. Your money is secured into a difficult insurance coverage product, and abandonment charges typically do not go away till you have actually had the policy for 10 to 15 years. Every long-term life insurance policy policy is different, however it's clear someone's general return on every dollar invested on an insurance item might not be anywhere near the reward price for the policy.

Private Family Banking Life Insurance

To provide an extremely basic and hypothetical instance, allow's think a person is able to gain 3%, on average, for every buck they spend on an "infinite banking" insurance policy item (after all expenditures and costs). If we think those bucks would certainly be subject to 50% in taxes total if not in the insurance item, the tax-adjusted rate of return could be 4.5%.

We assume greater than typical returns overall life item and a very high tax rate on dollars not put into the plan (that makes the insurance policy item look far better). The fact for lots of folks may be worse. This pales in contrast to the long-lasting return of the S&P 500 of over 10%.

Infinite financial is a fantastic product for agents that sell insurance, but might not be optimum when contrasted to the more affordable options (without any sales individuals making fat commissions). Here's a failure of some of the other purported advantages of boundless financial and why they may not be all they're gone crazy to be.

How To Be My Own Bank

At the end of the day you are purchasing an insurance policy item. We love the security that insurance coverage provides, which can be obtained a lot less expensively from a low-priced term life insurance policy. Overdue fundings from the policy may likewise minimize your survivor benefit, lessening one more level of security in the plan.

The principle only functions when you not only pay the substantial premiums, yet utilize additional money to purchase paid-up enhancements. The opportunity expense of every one of those bucks is incredible extremely so when you might rather be spending in a Roth IRA, HSA, or 401(k). Also when compared to a taxed investment account and even an interest-bearing account, infinite financial might not provide comparable returns (compared to spending) and comparable liquidity, accessibility, and low/no cost structure (contrasted to a high-yield interest-bearing accounts).

With the rise of TikTok as an information-sharing system, financial suggestions and strategies have actually located an unique way of dispersing. One such method that has been making the rounds is the limitless banking principle, or IBC for brief, amassing endorsements from celebrities like rap artist Waka Flocka Flame. While the approach is currently preferred, its roots map back to the 1980s when economist Nelson Nash introduced it to the world.

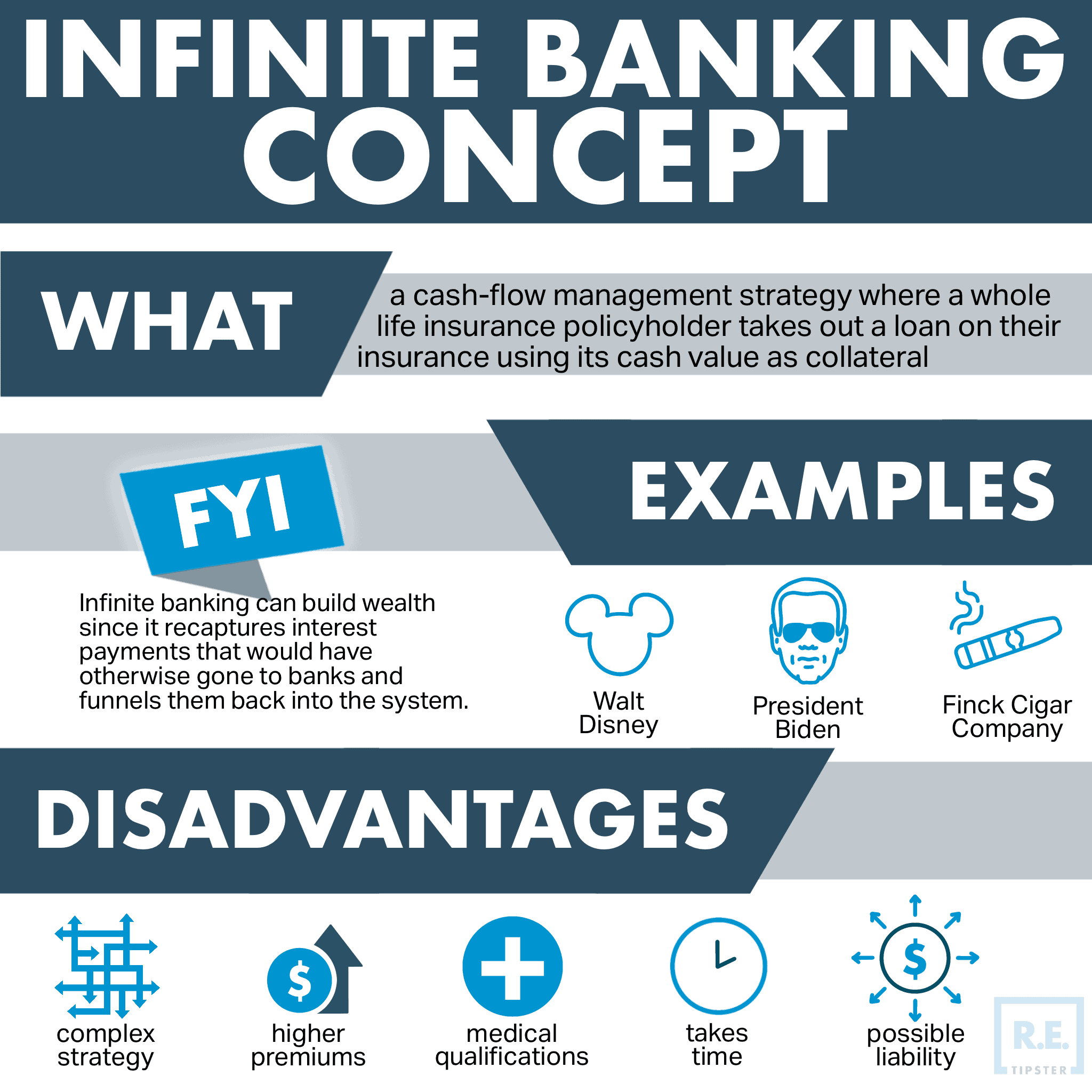

Within these policies, the cash money value grows based upon a price set by the insurer. Once a considerable money value accumulates, insurance policy holders can get a cash worth loan. These fundings vary from standard ones, with life insurance acting as security, meaning one might lose their coverage if loaning excessively without adequate cash money worth to support the insurance coverage expenses.

Wealth Nation Infinite Banking

And while the appeal of these plans is evident, there are inherent constraints and dangers, necessitating diligent cash value tracking. The technique's authenticity isn't black and white. For high-net-worth people or entrepreneur, particularly those utilizing methods like company-owned life insurance (COLI), the advantages of tax obligation breaks and compound development could be appealing.

The appeal of limitless banking doesn't negate its challenges: Price: The fundamental need, a permanent life insurance coverage plan, is costlier than its term counterparts. Eligibility: Not every person certifies for whole life insurance policy as a result of rigorous underwriting processes that can omit those with certain wellness or lifestyle problems. Intricacy and danger: The complex nature of IBC, coupled with its risks, may prevent many, especially when simpler and much less dangerous options are offered.

Alloting around 10% of your month-to-month earnings to the plan is simply not viable for lots of people. Utilizing life insurance policy as a financial investment and liquidity source calls for technique and monitoring of policy cash money worth. Seek advice from an economic expert to figure out if limitless banking straightens with your concerns. Part of what you check out below is just a reiteration of what has already been said over.

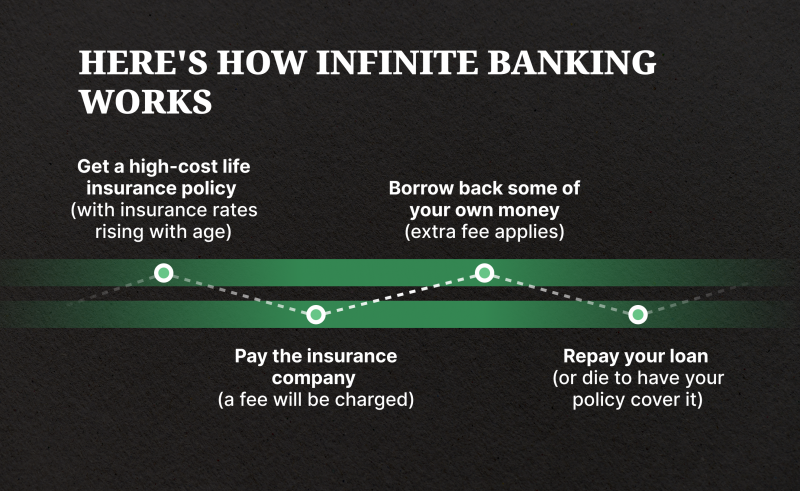

So before you get yourself right into a circumstance you're not planned for, know the complying with initially: Although the idea is commonly marketed thus, you're not actually taking a funding from yourself - how to set up infinite banking. If that held true, you would not have to settle it. Instead, you're obtaining from the insurance provider and have to repay it with passion

What Is Infinite Banking

Some social networks messages suggest utilizing money value from whole life insurance policy to pay down bank card financial obligation. The idea is that when you repay the finance with passion, the quantity will certainly be returned to your financial investments. Regrettably, that's not just how it functions. When you repay the car loan, a part of that passion mosts likely to the insurance provider.

For the initial a number of years, you'll be settling the compensation. This makes it incredibly hard for your policy to collect value during this time. Entire life insurance coverage prices 5 to 15 times more than term insurance. The majority of people simply can't manage it. So, unless you can afford to pay a couple of to a number of hundred bucks for the next years or more, IBC won't help you.

If you need life insurance, here are some beneficial suggestions to consider: Take into consideration term life insurance policy. Make certain to shop about for the best price.

Limitless financial is not a services or product provided by a details organization. Limitless financial is an approach in which you purchase a life insurance policy plan that accumulates interest-earning cash worth and get lendings versus it, "obtaining from on your own" as a source of resources. Then ultimately repay the finance and begin the cycle all over once more.

Pay plan costs, a portion of which constructs cash value. Take a financing out versus the policy's cash money worth, tax-free. If you use this concept as intended, you're taking cash out of your life insurance policy to purchase every little thing you 'd need for the rest of your life.

{kind=link}

Latest Posts

Whole Life Insurance Banking

Bank On Yourself Strategy

How To Start A Bank: Complete Guide To Launch (2025)